A practical guide for investors who want real estate-backed income without tenants, repairs, or market timing

When the housing market feels uncertain, most investors ask the same question:

“Should I buy, sell, or wait?”

It is a fair question.

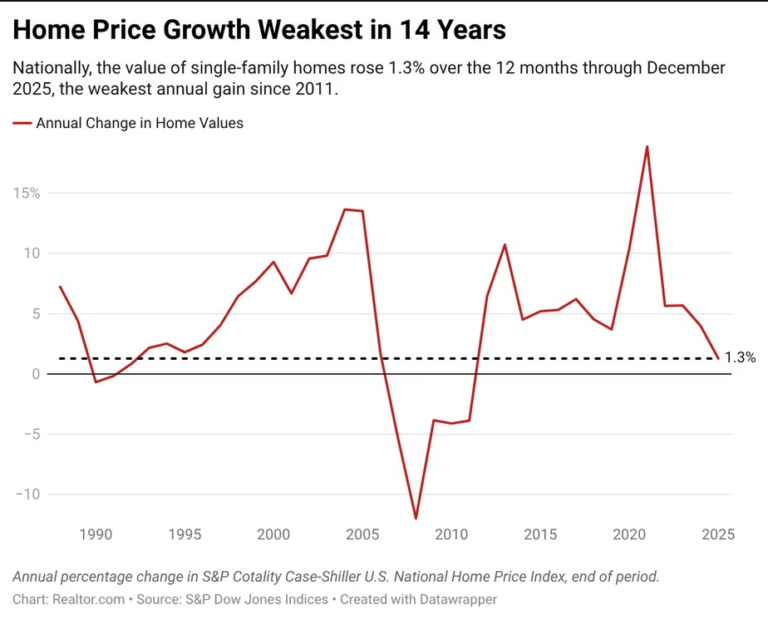

Home prices move. Interest rates change. Rents rise, flatten, or soften depending on the market. Some areas remain strong while others slow down. Headlines can make it feel like you either need to act immediately or stay frozen on the sidelines.

But there is a better question for long-term investors:

“How do I create steady income even when the market feels uncertain?”

That question changes everything.

Instead of trying to predict the next move in home prices, cash flow investors focus on getting paid consistently. Instead of hoping appreciation solves every problem, they look for investments backed by real assets, structured payments, and practical downside protection.

That is where mortgage note investing can become a powerful strategy.

At TLC Property Partners, we focus on real estate-backed income through mortgage notes. In simple terms, that means investors can participate in real estate without becoming landlords. Instead of owning the property, the investor owns the debt secured by the property.

You are not fixing toilets.

You are not chasing tenants.

You are not hoping the market rises next month.

You are focused on the monthly payment stream.

What Housing Uncertainty Really Means

Housing uncertainty does not always mean a crash.

It can mean:

- Buyers are hesitant because mortgage rates are higher

- Sellers are reluctant to lower prices

- Investors are unsure whether values will rise or fall

- Landlords are dealing with repairs, insurance, taxes, and tighter cash flow

- Rent growth slows in certain markets

- Affordability becomes difficult for everyday homeowners

In other words, uncertainty often means the market is harder to predict.

For investors who rely only on appreciation, this can create stress. If your entire strategy depends on buying a property today and selling it later at a higher price, then market timing matters a lot.

But cash flow investors think differently.

They ask:

- Is the borrower making payments?

- Is the loan secured by real estate?

- Is there enough equity protecting the investment?

- Is the monthly income attractive compared to the risk?

- Is the investment structured in a way that protects capital?

That is a very different lens.

Appreciation Is Nice. Cash Flow Is Necessary.

Many real estate investors have been trained to think appreciation is the prize.

Buy the house.

Wait for the value to rise.

Refinance or sell later.

That can work in a strong market. But it becomes much harder when values flatten or affordability tightens.

Cash flow is different.

Cash flow is not about waiting for a future sale. It is about income today.

For retirees, passive investors, and burned-out landlords, this matters. Monthly income can provide confidence. It can help cover expenses. It can reduce dependence on stock market swings. It can also make investing feel more practical and less emotional.

That is one of the reasons mortgage notes are attractive.

A performing mortgage note is designed to pay monthly principal and interest. The investor receives income from the borrower’s payment, while the property remains the collateral behind the loan.

The investor is not betting only on whether the property rises in value.

The investor is focused on the performance of the loan.

What Is Mortgage Note Investing?

Mortgage note investing means you are buying the debt secured by a property instead of buying the property itself.

Here is a simple example.

A homeowner has a mortgage. That mortgage includes:

- A loan balance

- An interest rate

- A monthly payment

- A repayment schedule

- A property securing the loan

When an investor buys the note, the investor steps into the lender’s position.

The homeowner keeps living in the property and continues making payments. A licensed loan servicer typically collects the payment, handles statements, tracks balances, and sends funds to the note owner.

The investor receives the income.

In plain English:

You are not buying the house. You are buying the right to receive the mortgage payments.

This is why people often say note investors “become the bank.”

Ready to Learn More?

If you want to understand how mortgage notes can create steady income backed by real estate, visit our Mortgage Note Investing page or schedule a conversation with TLC Property Partners.